Lululemon (LULU) at this price even with the challenges ahead too good to pass up

lululemon athletica inc. (LULU) is going through a very tumultuous time. The stock has been getting clobbered since hitting an all-time high of $511.29 on 12/29/2023 losing about 60% of its value since then. The reasons are plentiful for the collapse. Slowing US growth rates, tariff risk hurting margins, lack of product innovation and new competition (Vuori and Alo Yoga) in a fierce market resulted in Calvin McDonald stepping down as CEO. Search for a new CEO and a proxy fight that includes founder Dennis Wilson, who left the company back in 2015, has left the company focus fractured and a potential turnaround stalled due to this turmoil. Despite all these headwinds, there is an argument that now is a great time to buy shares at historically low multiples, a brand that still has loyal customers, and an ever-growing athleisure environment.

The Bullish Investment Thesis

1 – Growing Athleisure Market

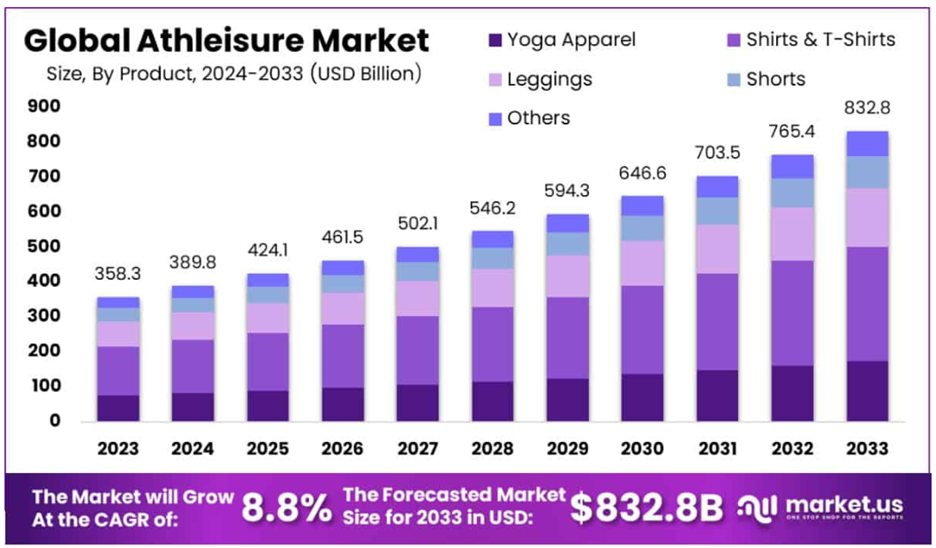

There are many reasons why I am bullish on lululemon as an investment. The entire athleisure market is still growing at a healthy clip. Anecdotally, just go outside during a weekend or evening and you can see many people wearing athleisure not just for the gym or sports but something to wear while running errands, traveling or meeting friends. This trend shows no signs of slowing either. Below is a charge showing the current athleisure market at around $338B in 2024 and expectations to grow up to $663B by 2030.

Source: Media Market

Though numbers vary depending on how large the athleisure market is, all projections show double digit growth rates for the next 5 years. lululemon in terms of market share is currently firmly in third place, behind Nike and Adidas. There are up and coming competitors Alo Yoga and Vuori that have been taking market share recently along with other smaller players including Wear Pact, Pangaia, Eileen Fisher and Outerknown.

Though lululemon is in third place, growth has been mixed. The Americas Market saw a contraction in Q3 of 2% which is very concerning as this market represents 75% of lululemon total revenue. One bright spot is the continual growth in international with revenue growth in China (up 46%) and rest of the world (up 19%) showing strong demand for lululemon products overseas. Projecting revenue growth for lululemon in the coming years hinges on the overall athleisure rising tide lifting all boats. For context, lululemon has averaged almost 20% positive revenue growth over the past 10 years and year over year growth of 10% even with the stagnant Americas market.

Another positive is the success of the Power of Three x2 initiative with the goal being to accelerate growth using product innovation, omni guest experience and market expansion. Men’s apparel growth has been strong in product innovation with an 8% increase year over year. Digital revenue growing at 13% is a healthy number and international revenue growth of 33% being very strong. Continued success in these endeavors is key to any discussion of a turnaround in the stock price.

2 – Strong Margins and Cheap Valuation

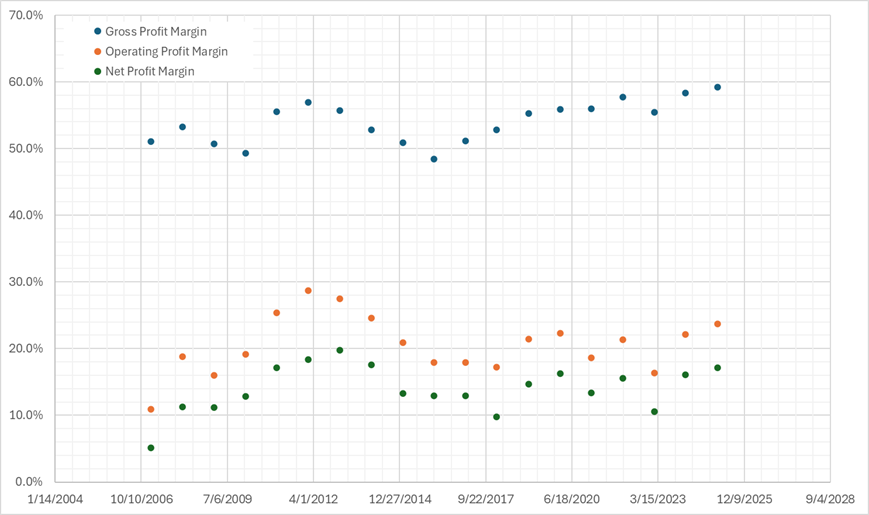

Rising revenue is not nearly as impactful if margins are being pressured. With such a drop in stock price, you would think the financials for lululemon would be deteriorating but the opposite is true. Below is a chart showing gross, operating and net profit margins since 2007. Margins are growing at a healthy clip showing that lululemon still has pricing power.

LULU Margin Rates from 2006 to 2025

The impact of tariffs will put pressure on margins, but this is company independent and will impact competitors along with lululemon. A strong balance sheet with over $1B in cash & cash equivalents and growing equity will help lululemon weather the uncertainty of tariffs.

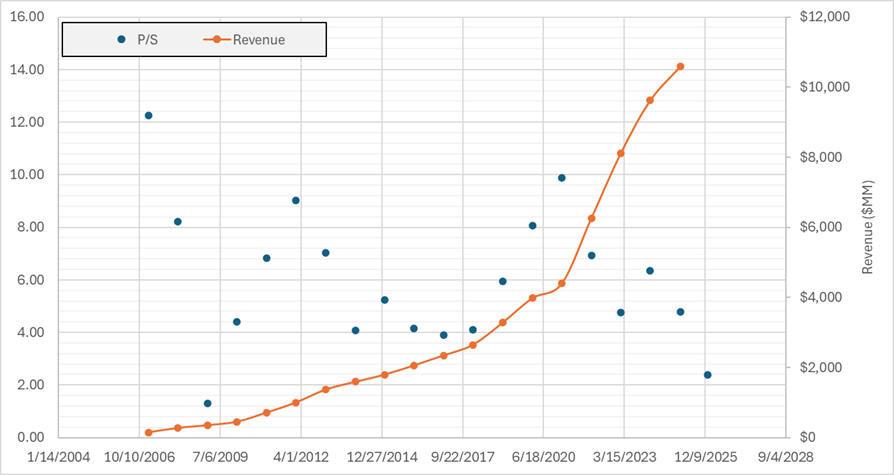

At current valuations, lululemon is trading at not just low multiples compared to their peers, but historically low compared to its own past performance. Below are three charts showing the price-to-earnings and price-to-sales ratios from 2007 to current levels.

LULU Price to Sales Compared to Revenue from 2006 to 2025

The price to sales ratio has not been this low since 2008 even with revenues growing consistently. lululemon management projects $11B for 2025 revenue or 4% growth compared to 2024.

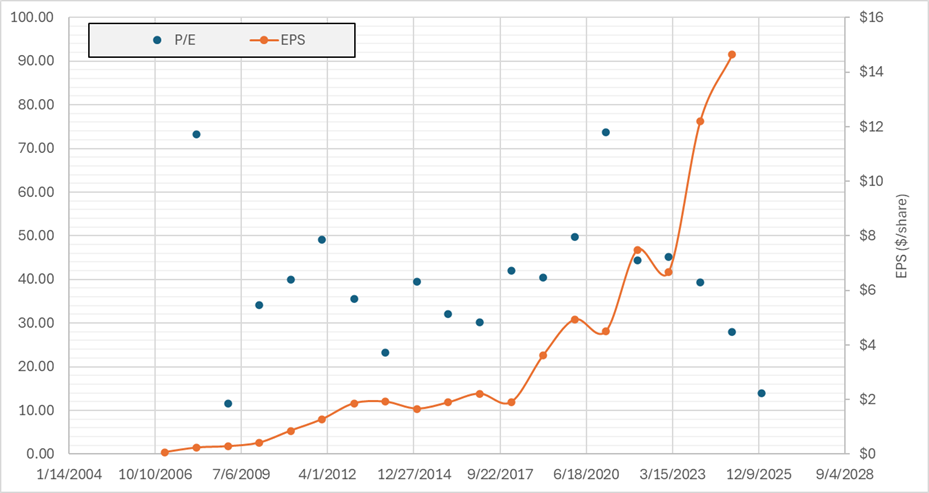

LULU Price to Earnings to EPS from 2006 to 2025

Over the past 4 years, the price-to-earnings ratio has been dropping precipitously to the multi-year lows currently seen at around 13 even with an overall strong EPS growth rate. For comparison, Nike has a forward P/E ratio of 42 and Adidas at 23 so lululemon is well below its main competitors. EPS has been growing with strong bottom-line growth and a shrinking share count with lululemon reducing share count on average by 2% per year and a 15% total share reduction since 2014. During Q3 2025 financial results, it was announced that the board of directors approved on Dec 3, 2025, another $1B for stock buybacks leaving a total of $1.6B currently earmarked for buybacks.

At these historically low multiples, some good news, a slight reversal in product innovation, Americas turnaround or even a great new CEO hire could spring the stock price much higher. Just with the CEO announcing stepping down resulted in an over 10% jump in one day.

Reasons To Be Cautious

Everyone knows about the tariff issues and the removal of the “de minimis provision” would hurt margins for all retailers including lululemon. Combined that with competition from above in Nike and Adidas and below with Vuori and Alo Yoga, lululemon needs to push product innovation as soon as possible and regain brand awareness and the “coolness” factor is has been lacking recently. There are two major issues I am focusing on, and they are inventory management and shrinking growth in the Americas.

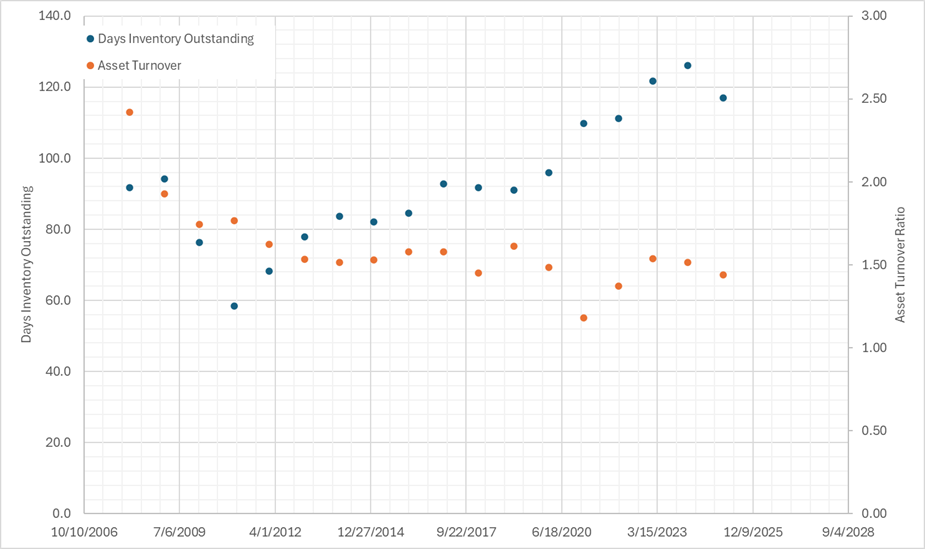

LULU Inventory Analysis

As shown in the chart above, the days inventory outstanding number has been slowly creeping higher, and it has been for a while now showing lululemon having difficulty moving product. Asset to turnover ratio showing the same result being lululemon not moving products to sales efficiently. Product innovation will help but that remains to be seen if that can turn these trends in a positive direction.

Another issue is that currently, the growth engine for lululemon is China and the rest of the world. There is a chance with current geopolitical trends that consumers become more domestically inclined with their shopping habits which could hurt lululemon, especially with respect to China. The numbers show that isn’t happening with healthy growth rates, but this is something to watch because if China growth rates slow down, this could be a big issue for lululemon moving forward.

Conclusion

Different reports have lululemon at somewhere between 4 – 7% of the athleisure market with Nike around 21% and Adidas at 15% (source). For the purposes of this analysis, using the above chart from market.us, and lululemon revenue, the market share grew from 1.4% to 2.5%. Based on conservative estimates, lululemon price target for 2033 is $401.99/share or an annualized return of 12.5% based on the following assumptions.

lululemon market share stays at its current estimate at 2.5% when trends over the past few years have lululemon rising relative to peers.

Revenue grew only due to rising overall market.

Profit margin of 15% is assumed, which is below current levels of 17% but trends with the 15-year average for lululemon.

Average share count reduction of 1%. Over the past 10 years, the share count for lululemon has dropped on average 2% yearly.

P/E ratio used was at currently reduced levels of 14.7. This P/E ratio represents a multi-year low for lululemon and is well below the 15-year average at 40. Even getting to a P/E ratio of 20 would result in the price target in 2033 jumping to $545.43 or an annualized return of over 20%.

lululemon just staying at the depressed valuations and current market share has the potential for substantial returns with solid margin for error while leaving room for actual results to surprise on the upside and increase that price target even higher.

As a current shareholder, I have been monitoring lululemon for a while now and adding/trimming shares to varying successes. The latest purchase being on 1/5/2026.

My Purchase History of LULU

lululemon stock in my view is very cheaply valued with a lot of bearish sentiment backed into the price. The concerns are not without merit but at these multiples, the potential for a great return with even a minor success catalyst, the risk to reward benefit is strongly on your side.